Are Indian VCs Becoming More Conservative?

April 14, 2026 by Sheikh MohammadThe Indian venture capital landscape is currently traversing a transformative period of recalibration, shifting from a cycle of exuberant capital deployment to one defined by structural maturity and operational rigor. To characterize this shift simply as a move toward "conservatism" would be an oversimplification; rather, the ecosystem is witnessing a transition toward "disciplined maturation" where capital is becoming increasingly selective, patient, and concentrated in high-conviction opportunities. While aggregate funding volumes in 2025 and early 2026 remain below the historic peaks of 2021, the underlying fundamentals of the market suggest a more resilient and sustainable growth architecture. This report examines the multi-faceted dynamics of this evolution, analyzing whether the perceived conservatism among Indian venture capitalists is a temporary reaction to global headwinds or a permanent structural shift toward a value-focused investment paradigm.

Macroeconomic Resilience and the Structural Shift in Capital Flow

The Indian economy in late 2025 and early 2026 continues to be a global outlier, maintaining a trajectory of strong fundamentals despite persistent geopolitical uncertainties and tighter global liquidity. The maturation of the venture capital (VC) market is inextricably linked to this broader economic resilience. Private equity (PE) and venture capital investments in India reached $\text{US } \$36.8 \text{ billion}$ across $1,506$ deals in 2025, marking a three-year high and indicating that capital is not scarce, but rather more discerning.

The transition from a "growth-at-all-costs" model to "sustainable unit economics" is the defining characteristic of the 2024–2026 cycle. This shift is supported by a robust growth architecture and rising institutional capacity, as highlighted in the Economic Survey 2026. Investors are now prioritizing "execution certainty" and "exit visibility" over speculative valuation expansion. This environment has forced a bifurcation in founder behavior, where successful entrepreneurs are those who have adapted to "burn efficiency" as a primary survival predictor.

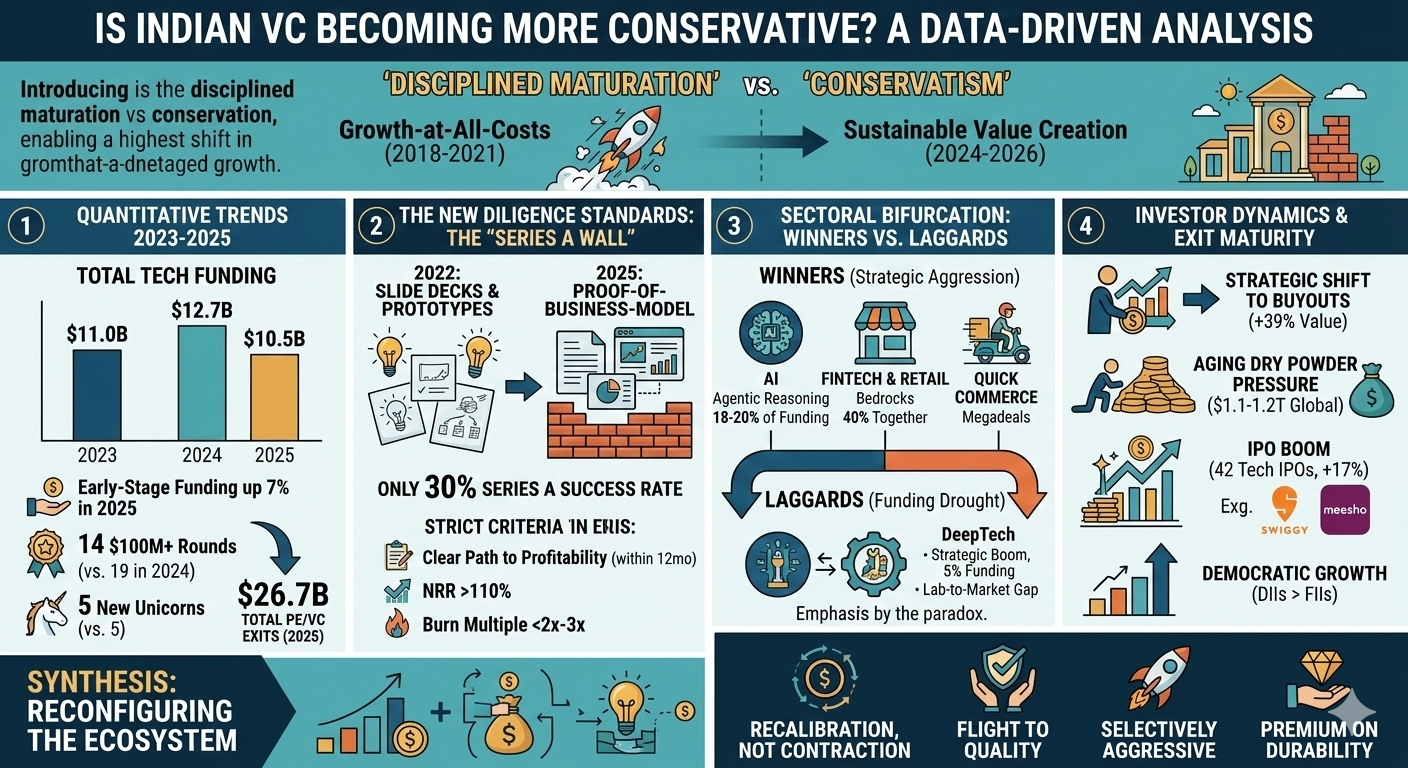

The Quantitative Reality of 2025–2026 Funding Cycles

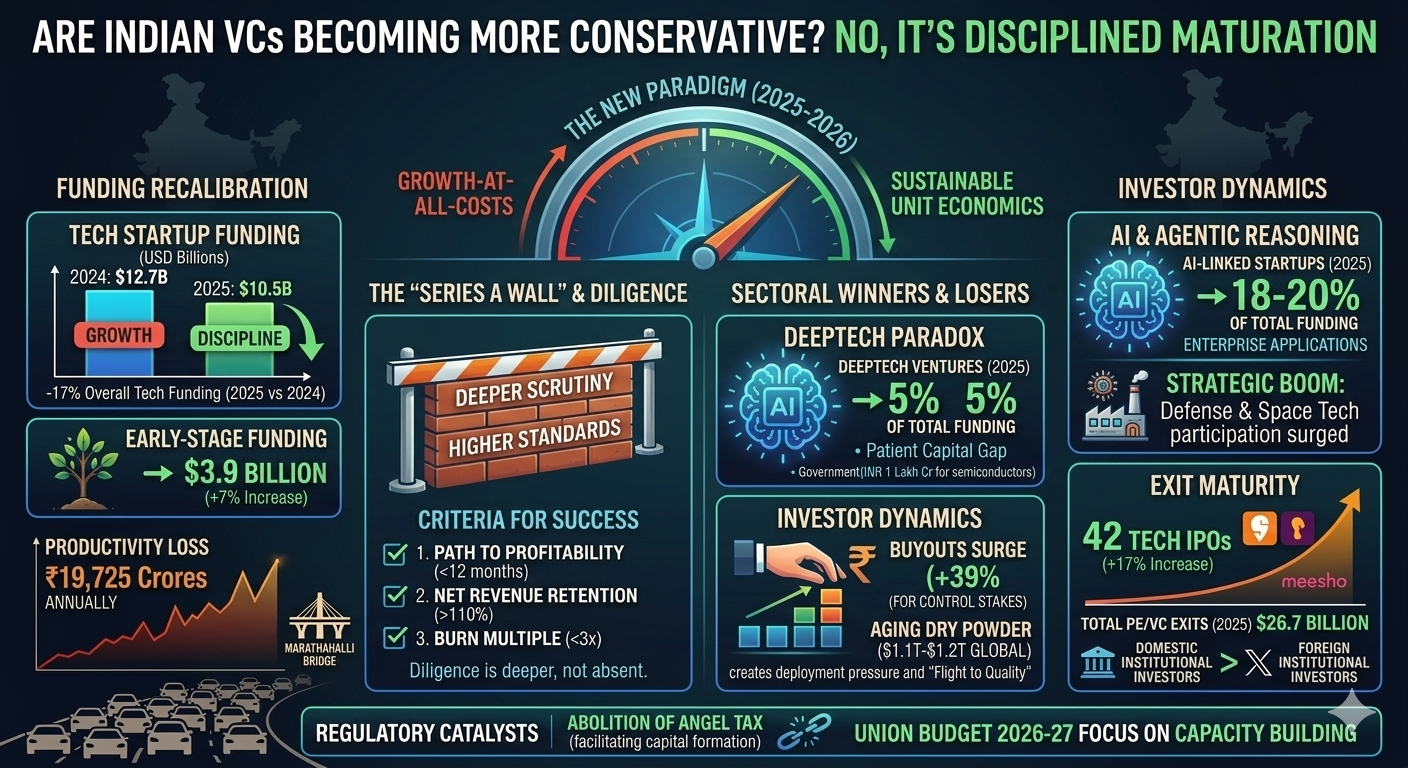

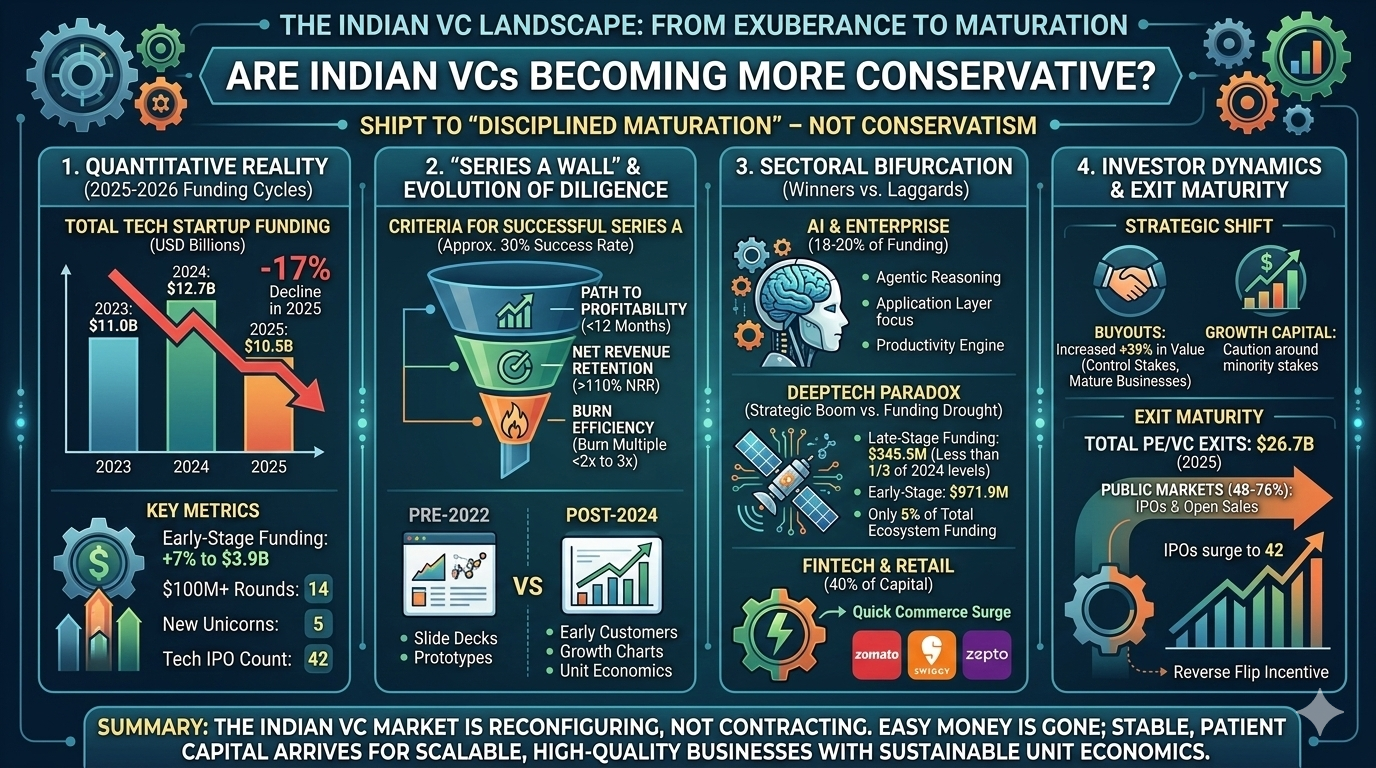

Analyzing the funding data from 2025 reveals a divergence between deal volume and deal value. While total funding in the tech startup sector saw a moderation—falling to approximately $\text{US } \$10.5 \text{ billion}$ from $\text{US } \$12.7 \text{ billion}$ in 2024—the broader PE/VC market remained buoyant. The following table illustrates the comparative performance of the Indian tech ecosystem over the last three fiscal periods.

Funding Metric (Tech Startups) | 2023 | 2024 | 2025 |

Total Funding (USD Billions) | $11.0$ | $12.7$ | $10.5$ |

Number of $100\text{M}+$ Rounds | $16$ | $19$ | $14$ |

New Unicorns Created | $2$ | $5$ | $5$ |

Tech IPO Count | $26$ | $36$ | $42$ |

Acquisitions | $153$ | $127$ | $136$ |

The $17\%$ decline in tech startup funding in 2025 compared to 2024 is often cited as evidence of VC conservatism. However, the resilience of early-stage funding and the sharp rise in IPO activity suggest a market that is stabilizing rather than contracting. Early-stage funding actually rose to $\text{US } \$3.9 \text{ billion}$ in 2025, a $7\%$ increase from the previous year, highlighting sustained investor confidence in scalable, growth-ready businesses.

Monthly Volatility and the "Stabilization" Narrative

The 2025 funding landscape was characterized by significant month-on-month volatility, reflecting the impact of global headwinds and a cautious "wait-and-watch" approach by international funds. For instance, October 2025 recorded $\text{US } \$5.3 \text{ billion}$ in PE/VC investments, a $9\%$ increase year-on-year, driven by large deals in financial services and e-commerce. However, the number of deals decreased to $102$, a $30\%$ decline month-on-month compared to September 2025, which saw $145$ deals.

Period | PE/VC Investment Value (USD) | Number of Deals | Key Large Deal (Example) |

October 2025 | $5.3$ Billion | $102$ | IHC acquiring Sammaan Capital ($1\text{B}$) |

November 2025 | $5.6$ Billion | $113$ | Brookfield acquiring Ecoworld ($1.5\text{B}$) |

The rise in average deal value during these months—despite fluctuating deal counts—underscores a shift toward fewer but larger transactions. This concentration of capital in "category leaders" and "defensible assets" is a hallmark of the current investment climate, as VCs move away from spreading small bets across a wide range of early-stage ventures.

The "Series A Wall" and the Evolution of Diligence Standards

One of the most profound changes in the Indian VC landscape between 2022 and 2026 is the dramatic shift in investor diligence. In 2022, companies were able to raise seed rounds based on slide decks and prototypes; by 2025, investors demanded early customers, growth charts, and clear unit economics even for seed-stage participation. This evolution has created what many founders call the "Series A Wall."

Benchmarking Success in a Selective Environment

In 2025, Series A became a "proof-of-business-model" round rather than just a milestone for product development. Across the ecosystem, only about $30\%$ of companies attempting a Series A raise in 2025 successfully closed their rounds. The criteria for success have become significantly more stringent, requiring founders to demonstrate:

Path to Profitability: A clear trajectory to reaching break-even within $12$ months, supported by improving unit economics data.

Net Revenue Retention (NRR): A threshold of above $110\%$ with expanding customer Annual Contract Values (ACV), meaning the customer base grows in value faster than the churn rate.

Burn Efficiency: A "Burn Multiple" (net burn divided by net new ARR) of below $2x$ to $3x$ is now considered healthy; anything above $4x$ is viewed as a significant risk unless growth exceeds $20\%$ month-on-month.

This rigor is not necessarily indicative of conservatism, but rather of a "quality reset". Investors have become more cautious with growth-stage capital after many "burnt their fingers" making flippant deals during the 2018–2021 funding rush. The current environment rewards "extreme ownership of outcomes" and "relentless iteration based on actual customer behavior" rather than creative extrapolation of market size.

The Credential Paradox and Founder Behavior

Interestingly, the traditional reliance on "credential-heavy" founder pairs—such as those from McKinsey, IIT, or IIM—has shown diminishing returns in 2025. Portfolio analysis comparing these founders against those without brand-name credentials revealed that the credentialed group did not consistently outperform. The determining factor for success in the 2025 environment was not pedigree, but the ability to adapt mental models quickly. Founders who ruthlessly prioritized revenue generation and cost reduction in early 2025 were far more likely to survive and raise follow-on capital than those waiting for a "return to normal".

Sectoral Bifurcation: The Winners and Laggards of 2026

Capital deployment in 2025 and 2026 has become highly sectoral, with certain industries attracting massive concentration while others face a structural "funding drought". The "Top-Funded Sectors" of 2025—Enterprise Applications, Retail, and Fintech—continued to draw the bulk of investor interest, but even these mature sectors saw year-on-year declines in total funding value.

The AI Inflection: From Generative Content to Agentic Reasoning

Artificial Intelligence (AI) has unequivocally established itself as the critical inflection point in 2026. The sector has transitioned from the era of "generative content creation" to the deployment of "highly autonomous, agentic reasoning systems". These mechanisms allow models to iteratively reason, self-correct, and navigate complex, long-horizon tasks—cognition traditionally associated with human expertise.

In India, AI-linked startups accounted for $18-20\%$ of total VC funding in 2025, with over $65\%$ of this capital directed toward the "application layer" and enterprise use cases. This contrasts with the global focus on more capital-intensive "foundational models". The Indian approach is characterized by:

Integration over Innovation: Positioning AI not as a standalone sector but as a "productivity engine" cutting across industries.

Sovereign AI and Infrastructure: A growing interest in India-specific sovereign AI investments and data center infrastructure, supported by long-term tax benefits in the Union Budget 2026.

Agentic Workflows: Funding for startups capable of building autonomous systems that can execute multi-day corporate workflows, mimicking human expertise in sectors like fintech and healthcare.

The DeepTech Paradox: A Strategic Boom vs. A Funding Drought

DeepTech—encompassing semiconductors, defense tech, space technology, and quantum computing—presents a stark paradox in the 2025–2026 ecosystem. While there is a "boom" in registrations—with India crossing $200,000$ registered ventures in December 2025—deep tech ventures attract only $5\%$ of total ecosystem funding.

DeepTech Metric (2025) | Performance Value | Context/Implication |

Late-Stage Funding | $\$345.5$ Million | Less than one-third of 2024 levels |

Early-Stage Funding | $\$971.9$ Million | Sustained interest in "lab-to-market" |

Government Commitment | $\text{INR } 1 \text{ Lakh Crore}$ | For semiconductors and AI infra |

Patent Commercialization | $15\%$ | Significant execution failure vs. Israel ($90\%$) |

The "structural divide" in DeepTech is driven by a lack of "patient, mission-aligned capital" required for long R&D cycles. Legacy funding models still prioritize quick returns over deep innovation. Furthermore, regulatory bottlenecks have compounded the issue; for example, the "Fund of Funds 2.0," which earmarked $\text{INR } 10,000 \text{ crore}$ for deep tech in April 2025, remained without implementation guidelines nine months later. Despite these challenges, strategic sectors like defense and space are moving from the "fringes to the mainstream," with a $17\%$ jump in defense capital outlay in the 2026 budget reinforcing the role of private players.

Fintech, Retail, and the Quick Commerce Surge

Fintech and Retail remain the "bedrocks" of the Indian startup economy, together accounting for nearly $40\%$ of total capital deployed. However, the nature of investment in these sectors has changed. In 2025, there was a shift from "speculative valuation expansion" to "operational value creation".

Within e-commerce, Quick Commerce emerged as a breakout theme in 2024–2025. Rapid customer adoption and "demonstrated paths to profitability" conferred credibility on the business model, leading to megadeals for players like Zepto and Swiggy. By early 2026, large players began a "10-minute food delivery race," with BigBasket planning a nationwide service to challenge Zomato and Swiggy.

The Regulatory Renaissance: Facilitating Maturity Through Policy

The period of 2024–2026 has been marked by significant regulatory reforms aimed at bolstering the Indian startup ecosystem and attracting foreign capital. The most celebrated of these was the abolition of the "Angel Tax" in July 2024, effective for all classes of investors from the financial year 2025–2026.

The Impact of Angel Tax Abolition

For over a decade, the Angel Tax (Section 56(2)(viib)) was a source of distress for startups, treating investments above the "fair market value" as taxable income. Its removal has eliminated a significant barrier to capital formation and reduced valuation disputes with tax authorities.

Before Abolition: Investors preferred DPIIT-recognized startups or SEBI-registered AIFs to avoid exposure; valuation mismatches often triggered tax notices and prolonged negotiations.

After Abolition (From April 2025): There is broader participation; investors can fund any unlisted company without Angel Tax exposure, leading to smoother cross-border flows and improved "ease of doing business".

However, the regulatory environment is not without mixed signals. The increase in Long-Term Capital Gains (LTCG) tax to $12.5\%$ and Short-Term Capital Gains (STCG) to $20\%$ in recent budgets has sent a "recalibration" signal to the investment community, balancing the ease of entry with higher taxation on exits.

Union Budget 2026–2027: Focus on Capacity Building

The Union Budget 2026–2027 further emphasizes "long-term capacity building" rather than short-term sentiment management. Key provisions include:

New Income Tax Act 2025: Coming into effect in April 2026, aiming to simplify rules and reduce the "multiplicity of proceedings".

SME Growth Fund: A $\text{INR } 10,000 \text{ crore}$ fund to create the "champions of the future" among MSMEs.

Deep Tech and AI Incentives: Tax holidays for foreign companies using Indian data centers and higher allocations for IT and telecom to accelerate specialization in the AI compute value chain.

Rationalization of Buyback Tax: Proposed to be taxed as capital gains instead of dividend income, providing relief to shareholders and promoters during consolidation events.

Investor Dynamics: The Rise of Buyouts and Dry Powder Management

The "fundraising paradox" of 2025—where deal volume hit a high while fundraising fell to $\text{US } \$10.4 \text{ billion}$—reflects a market where fund managers are choosing to aggressively deploy "accumulated dry powder" rather than raising fresh capital amid uncertain global markets.

The Strategic Shift Toward Buyouts

A clear strategic pivot occurred in 2025, as investors increasingly preferred "control stakes" in mature businesses over minority positions in high-growth but volatile startups. Buyout deals surged $39\%$ in value in 2025, reflecting a maturing PE/VC market where operational control and governance improvements are prioritized.

Strategy Shift | 2024-2025 Trend | Underlying Reason |

Buyouts | Increased $+39\%$ in Value | Preference for ownership and influence |

Growth Capital | Decreased / Softened | Caution around minority stakes in high-burn tech |

PIPE Deals | Volatile (High in Oct 2025) | Driven by deep liquidity in public markets |

Credit Deals | Rising Resilience | Used to manage liquidity and bridge valuation gaps |

This focus on "pure-play buyouts" is particularly evident in tech-enabled services, healthcare, and financial services, where platform scalability and cash-flow visibility allow for "hands-on value creation".

Dry Powder Aging and Deployment Pressure

As of mid-2025, global private equity sponsors were sitting on a "staggering" $\text{US } \$1.1 \text{ trillion to } \$1.2 \text{ trillion}$ in dry powder. Crucially, more than $40\%$ of this capital has been available for over two years—the highest level in nearly a decade. This "aging" dry powder is creating significant deployment pressure on General Partners (GPs), who must put capital to work within their four-to-five-year investment timelines.

This pressure is colliding with a "limited supply of resilient assets," fueling a "flight to quality". GPs are willing to pay "premium multiples" for durability and downside protection. In 2025, the median EBITDA multiple for global buyout deals reached a record $11.8x$, marginally surpassing the 2022 high. In the Indian context, this has translated to a "concentration of capital" in fewer, higher-quality startups, which explains why average deal sizes grew even as total funding volumes moderated.

Exit Maturity: The IPO Boom as a Catalyst for Liquidity

The most significant "bright spot" in the 2024–2026 cycle has been the maturation of India's exit environment. For years, the lack of exits was the primary criticism of the Indian VC market; however, 2025 has redefined India as a "market that offers multiple viable routes for exit".

The Dominance of Public Markets

Total PE/VC exits rose to approximately $\text{US } \$26.7 \text{ billion}$ in 2025, with public market exits (IPOs and open market sales) accounting for nearly $48\%$ to $76\%$ of total exit value.

The IPO Surge: India saw $42$ tech IPOs in 2025, a $17\%$ increase over 2024 and a $62\%$ rise compared with 2023. Major listings included Swiggy, Meesho, Aequs, and Ravel.

The "Reverse Flip" Incentive: High valuations in the Indian secondary market have driven a trend of "reverse flipping," where companies previously domiciled abroad are choosing to list in India to capitalize on strong domestic investor appetite.

Democratic Growth: For the first time, Domestic Institutional Investors (DIIs) have surpassed Foreign Institutional Investors (FIIs) in NSE-listed companies, providing a stable capital base for new-age tech listings.

The success of these public market entries has shifted the late-stage VC appetite. Founders are now considering public listings "earlier," viewing an IPO as a "viable alternative to large late-stage private funding". This has led to a deceleration in mega-rounds (rounds of $\text{US } \$100 \text{ million}$ or more), as companies opt for "pre-IPO rounds" or head straight to the public markets to avoid private valuation friction.

Strategic M&A and Consolidation

While the IPO market surged, strategic M&A activity showed mixed but significant trends. India recorded $136$ tech acquisitions in 2025, a $7\%$ increase from 2024. The largest transaction was Diginex’s $\text{US } \$2.0 \text{ billion}$ acquisition of Resulticks, highlighting a "renewed confidence among corporates" to buy innovation rather than building it internally. In sectors like healthcare, M&A deal volumes increased by $82\%$ in 2025, signalling consolidation-driven growth even as private equity funding remained constrained.

Synthesis: Are Indian VCs Becoming More Conservative?

The evidence suggests that the "conservatism" narrative is a misinterpretation of a "disciplined maturation" process. While it is true that investors have become more selective and risk-averse at certain stages, they remain "selectively aggressive" in high-potential, high-conviction sectors.

Dimensions of Modern VC Discipline

The "conservative" elements of the current cycle are focused on Financial Hygiene and Valuation Rationalization:

Stage-Wise Selectivity: Seed-stage funding saw a $30\%$ drop in value in 2025, as investors moved away from speculative bets toward "traction-proven" startups.

The "Quality Filter": The average size of megadeals fell by $20\%$ as investors shifted toward "conservative valuations" and "defensible unit economics".

Burn Rate Scrutiny: The "growth-at-all-costs" era has been replaced by a focus on the "Burn Multiple," where high-burn companies are effectively locked out of growth-stage capital.

Dimensions of Strategic Aggression

Conversely, VCs are behaving aggressively in areas of Long-Term Strategic Value:

AI Integration: AI-native and AI-first startups attract nearly $20\%$ of total funding, with investors doubling down on "agentic reasoning" systems that promise immediate enterprise ROI.

Early-Stage Conviction: Early-stage funding (Series A/B) rose $7\%$ in 2025, indicating that "patient capital" is still eager to back the next generation of category leaders.

Buyout Dominance: The $39\%$ surge in buyout value demonstrates a willingness to deploy massive amounts of capital for "operational control" and "platform building" in mature sectors.

DeepTech and Manufacturing: Despite the "funding drought" in late-stage deep tech, early-stage participation in semiconductors, defense, and space tech has surged, driven by government policy and the "Pax Silica" supply chain realignment.

The 2026 Trajectory: A Market Defined by Execution

As 2026 progresses, the Indian venture capital market is entering a "year of execution". The focus has moved from "managed optics" to "actual capacity building". Several factors will define the remainder of the 2026 cycle:

The Federal Reserve Effect: Year-end rate cuts in late 2025 have begun lowering the "cost of capital," encouraging sponsors to move beyond "window shopping" and actively deploy their record levels of dry powder.

Public Market Integration: The virtuous cycle of IPOs and secondaries will likely continue to provide the liquidity needed to reassure LPs and attract fresh capital commitments, even as fundraising for new funds remains a "bottleneck".

The "Valley of Death" in DeepTech: The primary challenge for the ecosystem remains the "lab-to-production" transition for capital-intensive ventures. Success in 2026 will depend on whether government-backed initiatives like the "Fund of Funds 2.0" can effectively bridge this gap with "mission-aligned capital".

The Maturity of "Bharat-VISTAAR": The expansion of the startup ecosystem beyond the "Golden Triangle" (Bengaluru, Mumbai, Delhi-NCR) into Tier-II cities like Jaipur and Ahmedabad will test the scalability of India's digital public infrastructure and the depth of its regional innovation hubs.

In conclusion, the Indian venture capital market is not contracting; it is reconfiguring. The "conservative" behavior observed is a necessary correction after a period of excess, resulting in a healthier, more mature ecosystem that rewards "durability and downside protection". For founders, the era of "easy money" is gone, but the era of "stable, patient capital" has arrived for those capable of building scalable, high-quality businesses with "sustainable unit economics". The Indian startup story in 2026 is no longer about "catching up" to global benchmarks; it is about "setting the standard" for execution in a volatile world.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →